HELY5: Why Aren’t Americans Buying Electric Cars?

Hákon Explains Like You’re 5

Everyone has an answer to this question. The experts, the analysts, the think tanks — they’ve all got their theories. Let me walk you through them, and then let me show you why they’re almost all wrong.

The Official Story

Here’s what you’ll hear if you ask a Very Serious Person why Americans aren’t buying EVs:

“They’re too expensive.” The average EV costs 25–30% more than the average car. Most Americans want something under $45,000, but only about 14% of EV models hit that price point (PwC eReadiness Study, 2024).

“There’s nowhere to charge them.” 56% of Americans cite lack of charging stations as a concern (AAA EV Survey, 2025).

“They can’t do long trips.” 57% of people say EVs aren’t suitable for long-distance travel (AAA, 2025).

“Battery costs are still too high.” The raw materials are expensive. The supply chains aren’t mature. Give it a few more years.

These sound reasonable, right? Each one sounds like a real problem. Put them all together and you’ve got a pretty convincing story about why EV adoption in America is stuck at around 8% while China just crossed 50%.

There’s just one small problem.

One Car Destroys the Narrative

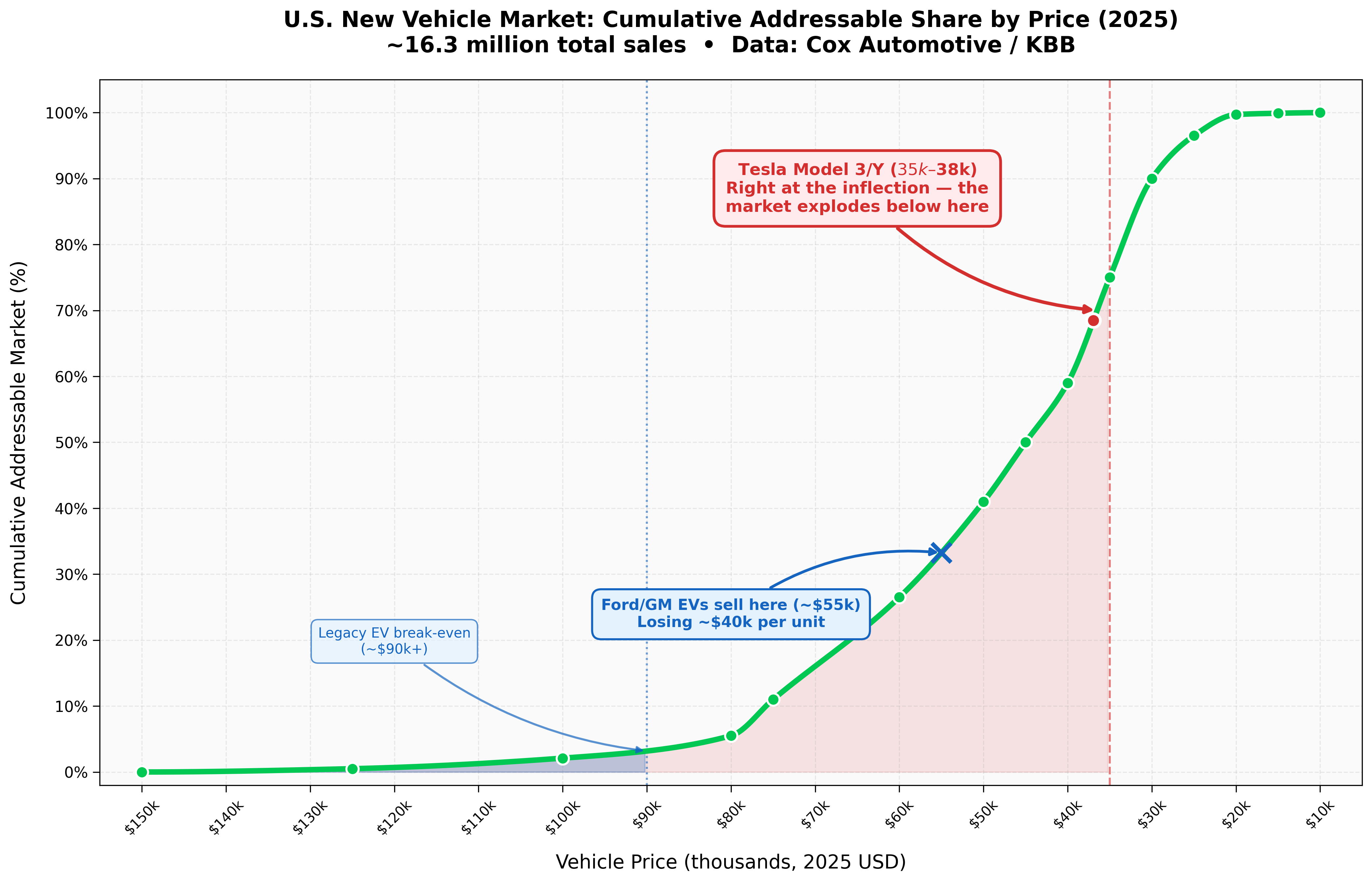

Tesla sells the Model 3 starting at about $35,000 and the Model Y at about $38,000.

They are profitable at these prices.

They are manufactured in America.

They are, by most measures, the most American-made cars on the road.

Now go back through the list.

“EVs are too expensive” — Tesla sells two models in the price range where 45% of American car demand lives, and makes money doing it.

“Battery costs are too high” — if pack costs were prohibitive, Tesla couldn’t profit at $35k. They’re not losing money and hoping to make it up in volume. The unit economics work. Right now.

“There’s nowhere to charge them” — Tesla built the Supercharger network: over 70,000 connectors, 99.95% uptime, three out of four fast chargers in North America (Tesla NACS). And it’s no longer Tesla-exclusive — every major automaker has adopted Tesla’s NACS standard, and the network is open to Ford, GM, Hyundai, BMW, Mercedes, and essentially everyone else as of 2025 (Consumer Reports, 2025). Charging is a solved problem.

“They can’t do long trips” — a Model Y does 300+ miles on a charge. The average American drives 31 miles a day (AAA Foundation, 2024). The long-distance concern is anchored to the twice-yearly road trip while ignoring the 363 other days of the year — and even those road trips work fine with the Supercharger network.

So affordable EVs exist. They’re profitable. They’re made in America. The charging network is built, open, and reliable. And people know about them — Tesla is one of the most recognizable brands on earth.

Which raises the question nobody in the mainstream seems to want to ask.

The one they all keep dodging.

If the product exists and the market should want it, why isn’t the rest of the American auto industry building competitive alternatives?

The Answer Nobody Talks About

The problem isn’t demand. The problem isn’t batteries. The problem isn’t charging.

The problem is that General Motors and Ford cannot build EVs efficiently, and the reason they can’t has nothing to do with technology.

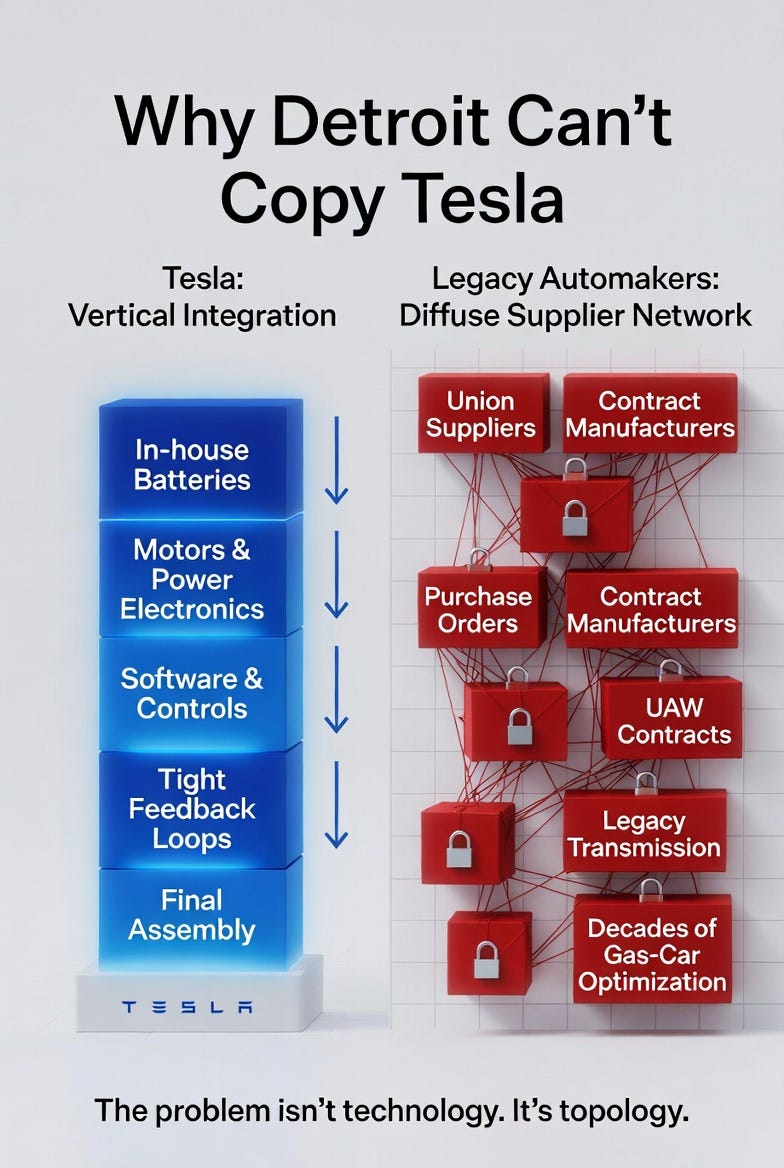

Here’s how Tesla builds cars: they make their own batteries, their own motors, their own power electronics, their own software, and they assemble all of it under tight vertical integration. When something isn’t working, the engineer who designed it is in the next building. Feedback loops are tight. Iteration is fast. Costs are controlled at every layer.

Here’s how GM and Ford build cars: they contract out to hundreds of suppliers scattered across the country. The transmission comes from here. The electronics come from there. The seats come from somewhere else. It’s a vast, diffuse network of independent companies all connected by contracts and purchase orders.

This network was built for internal combustion engines. It was optimized, over decades, for making gas cars. And it is spectacularly bad at making electric cars.

This isn’t a mystery. Ford has publicly reported losing over $40,000 on every EV it sells. Not because EVs are inherently expensive to build — Tesla proves they’re not — but because Ford’s organizational structure can’t produce them efficiently. The car isn’t the problem. The network of contractual obligations building the car is the problem.

So Why Don’t They Reorganize?

They can’t.

The United Auto Workers union has spent decades locking in contracts that distribute manufacturing across a web of unionized suppliers. These contracts dictate who builds what, where, and for how much. Bringing those steps in-house — which is exactly what you’d need to do to compete with Tesla’s vertical integration — means breaking those contracts and eliminating those jobs. Ford’s CEO Jim Farley understands this. He split Ford into three divisions specifically to make the cost disease visible. That’s the move of someone who sees the problem clearly but is legally constrained from solving it.

GM’s leadership, meanwhile, is still celebrating record Tahoe sales while the Blazer EV’s sales dropped 77% in Q4 2025. They sold 23,115 Blazer EVs the entire year (WardsAuto, 2026). Tesla sold more Model Ys than that in a slow week.

Cost Curves and Inevitability

Here’s what makes this fatal: the number of people who can afford a car doesn’t grow linearly as prices fall. Almost nobody buys a $60,000 car. A meaningful chunk of people buy $45,000 cars. More than half the market lives below $35,000. The total addressable market explodes as you move down the price curve — it’s a reverse power law.

Tesla is already touching the zone where the market gets enormous. Every dollar they shave off from here expands the pool of potential buyers super-linearly. Legacy automakers, trapped in a cost structure that can’t produce EVs below $50k without hemorrhaging cash, are locked out of the part of the curve where almost all the customers live.

The Punchline

The market caps tell the whole story.

Tesla: $1.47 trillion.

General Motors: $77 billion.

Ford: $56 billion.

Stellantis: $24 billion.

GM does $185 billion in revenue. Ford does about the same. They sell millions of vehicles. And the market values them at roughly a third of one year’s revenue — which is basically the liquidation value of their truck franchises plus their finance arms.

Every “explanation” for slow EV adoption — price, range, charging, consumer sentiment — is a downstream symptom of incumbent manufacturers being structurally incapable of competing with a vertically integrated competitor. The demand would follow if the products and prices were there. The products and prices can’t get there through the existing industrial architecture.

Detroit didn’t die because of technology. It died because of topology.

The market has already priced in the death. The corpse just hasn’t reached thermal equilibrium.

HELY5 is a series where I take ideas that matter and explain them without jargon, pretension, or hand-waving. If you learned something, subscribe and share.